ToughBuilt Industries Inc. $TBLT Company Analysis

On July 18, 2024 at market open, ToughBuilt Industries Inc. securities will be delisted and suspended from trading on the Nasdaq Stock Market. Trading will move to the Over The Counter (OTC) market.

Company Overview

ToughBuilt designs and engineers (innovates) all their hand tools, bags, pouches, saw horses & work benches, and modular storage in the USA, sources them globally from China, India and the Philippines (and a little in Mexico), and sells them through global home improvement retailers like Home Depot, Lowe's and Menards, professional trade suppliers, smaller home improvement retailers, and on Amazon. They focus on non-powered tools.

ToughBuilt designs and engineers (innovates) all their hand tools, bags, pouches, saw horses & work benches, and modular storage in the USA, sources them globally from China, India and the Philippines (and a little in Mexico), and sells them through global home improvement retailers like Home Depot, Lowe's and Menards, professional trade suppliers, smaller home improvement retailers, and on Amazon. They focus on non-powered tools.

- They sell heavy-duty, modular, mobile tool storage (new StackTech TM) and Massive Mouth TM tool bags.

- They sell long-lasting tool bags, belts and pouches, business organizers, and knee pads.

- They sell metal goods such as hammers, saw horses, knives, screwdrivers, saws, snips, and levels.

- They sell electronics like a distance finder, angle finder, and a room laser leveler.

Company Financial Discussion

The Current Situation:

This is a young, high-growth, small capitalization, technology company focused on design, procurement, marketing and placement of product in retail channels. Their revenues have grown from $1 million not that long ago to around $100 million currently, with fluctuations around the decline of the U.S. housing and home improvement market.

The company has never made a profit. The company is focused on growth. The company has used significant amounts of cash. Until Q2 2024, they funded working capital needs with equity by repeatedly diluting their equity shareholders to raise progressively smaller amounts. Their last equity recapitalization raised ~$4 million in February 2024 after the company was valued at ~$1 billion in the past.

The Promise:

The company drew a line in the sand during the February 2024 equity raise and decided to focus on breaking even on an operating basis by earning positive Cash Flow From Operations (CFFO) in Q3 2024. This required significant cost reduction while maintaining or increasing revenue from product shipments to retailers. We believe they can achieve positive CFFO in Q3 2024.

The Issue:

We have not seen current financials since September 30, 2023. We are waiting for the 2023 10-K and the March 31, 2024 10-Q financial statements. They have not been filed although we have assurances they will be done as soon as possible, and the results will not be materially different than in the past. Part of the most recent delay 'stems from the implementation of a new financial accounting software system on January 1, 2023.'

Operating performance in the field looks good to us, with increased sales and promotions at Menards in Q2 and steady replenishment of StackTech at Lowe's. Bills of lading show near-weekly shipments to U.S. retailers. ToughBuilt reduced their real estate footprint, arranged $30M+ in purchase order financing, implemented layoffs and executive pay cuts, and settled two lawsuits resulting from real estate cost reduction. We like the frugality.

In their last financial report, their total debt was around $1 million and amortizes regularly, which seems manageable.

The lack of financial statements into July 2024 has raised our level of concern with transparency, financial controls, SOX compliance, solvency, IT systems and data security, and appropriate levels of staffing and auditing for a publicly traded company.

Nasdaq Listing Qualifications department decided to delist the company's securities due to three separately named issues:

We contacted NASDAQ but they stated that it is the Company's responsibility to inform shareholders of the status of their listing.

The Current Situation:

This is a young, high-growth, small capitalization, technology company focused on design, procurement, marketing and placement of product in retail channels. Their revenues have grown from $1 million not that long ago to around $100 million currently, with fluctuations around the decline of the U.S. housing and home improvement market.

The company has never made a profit. The company is focused on growth. The company has used significant amounts of cash. Until Q2 2024, they funded working capital needs with equity by repeatedly diluting their equity shareholders to raise progressively smaller amounts. Their last equity recapitalization raised ~$4 million in February 2024 after the company was valued at ~$1 billion in the past.

The Promise:

The company drew a line in the sand during the February 2024 equity raise and decided to focus on breaking even on an operating basis by earning positive Cash Flow From Operations (CFFO) in Q3 2024. This required significant cost reduction while maintaining or increasing revenue from product shipments to retailers. We believe they can achieve positive CFFO in Q3 2024.

The Issue:

We have not seen current financials since September 30, 2023. We are waiting for the 2023 10-K and the March 31, 2024 10-Q financial statements. They have not been filed although we have assurances they will be done as soon as possible, and the results will not be materially different than in the past. Part of the most recent delay 'stems from the implementation of a new financial accounting software system on January 1, 2023.'

Operating performance in the field looks good to us, with increased sales and promotions at Menards in Q2 and steady replenishment of StackTech at Lowe's. Bills of lading show near-weekly shipments to U.S. retailers. ToughBuilt reduced their real estate footprint, arranged $30M+ in purchase order financing, implemented layoffs and executive pay cuts, and settled two lawsuits resulting from real estate cost reduction. We like the frugality.

In their last financial report, their total debt was around $1 million and amortizes regularly, which seems manageable.

The lack of financial statements into July 2024 has raised our level of concern with transparency, financial controls, SOX compliance, solvency, IT systems and data security, and appropriate levels of staffing and auditing for a publicly traded company.

Nasdaq Listing Qualifications department decided to delist the company's securities due to three separately named issues:

- Company is not in compliance with Nasdaq’s majority independent board and independent committee requirements, as outlined in Listing Rules 5605(b), 5605(c)(2)(A)(i) and (ii), 5605(d)(2)(A), and 5605(e)(1)

- Company's failure to timely file its Form 10-K for the year ended December 31, 2023

- Company's failure to timely file its Form 10-Q for the period ended March 31, 2024, pursuant to Listing Rule 5250(c)(1).

We contacted NASDAQ but they stated that it is the Company's responsibility to inform shareholders of the status of their listing.

Circling back to the core, fundamental financial issue, the company generates about $25M in gross margin on $100M in revenue per year, and prior to this point expenses exceeded that amount. If the company can live within the $25M operating budget, it can retire its debt and continue to invest. If the company increases gross margins (either increasing margin percentages or total revenue), then it grows its maximum operating budget.

Marcum LLP is the independent auditor for ToughBuilt Industries, Inc.

- Marcum LLP provides independent auditing services to the company and serves as an 'Expert' on the company's financials in S-3 registration statements. They offer these services out of their Costa Mesa, California office, 600 Anton Boulevard, Suite 1600. Costa Mesa, CA 92626. The office managing partner is Philip J. Wilson, CPA licensed by the State of California, (949) 236-5650, They have been providing financial statement audits since at least 2018. William N. Haddad, CPA licensed by the State of California, is a Director of Assurance, (949) 236.5629.

- We have repeatedly contacted Mr. Wilson, CPA (by phone and email) to confirm that Marcum LLP is still the auditor of ToughBuilt and have not received a reply.

ToughBuilt Videos

Here are a few videos to give a sense of the company's marketing and positioning.

Here are a few videos to give a sense of the company's marketing and positioning.

Work environment; What it is like to work there

My sense is of a technology incubator / startup / fast-paced firm that pays well, but expects teams to create innovative tool designs that are brought through production and global distribution.

There is one job opening at Toughbuilt in-person at Irvine, CA today:

We recently reviewed online reviews by self-declared, but unverified current and previous employees.

Key takeaways:

Source: Job reviews and job descriptions we could view for free, get our hands on, for free and without signing up. This included Glassdoor dot com (thank you).

My sense is of a technology incubator / startup / fast-paced firm that pays well, but expects teams to create innovative tool designs that are brought through production and global distribution.

There is one job opening at Toughbuilt in-person at Irvine, CA today:

- Global sourcing buyer (open, $90k to $100k, the range comes from another website, not ToughBuilt Careers.)

We recently reviewed online reviews by self-declared, but unverified current and previous employees.

Key takeaways:

- A fast-paced environment with high expectations. People are expected to work nights, weekends and travel for business when needed. This is not an early-morning office.

- People liked the culture, and the chance to work with passionate, committed, driven design experts.

- People liked the office and coffee/food perks. People work in the office.

- Pay and benefits are good. More than competitive.

- Few human resources formal processes (e.g., annual reviews).

- Solid design shop. They win design awards for innovation.

- Tool developers own the process end-to-end (we infer this).

- No formal project management processes and no micromanagement.

- Opportunities to create cool and innovative products.

- There is always more to do as someone completes a project. The demand for design work is there.

- The company recently laid off ~20 workers.

- This is a high-growth environment and that can be tough on the organization.

Source: Job reviews and job descriptions we could view for free, get our hands on, for free and without signing up. This included Glassdoor dot com (thank you).

There are a few ideas from the Global Sourcing Buyer job description that stand out for us:

- ToughBuilt Industries serves the professional trades by delivering extraordinary products through a Southern California-based technological incubator.

- We have an ardent and growing community of pros and enthusiasts, and have earned technical awards, rave reviews, and formed a global community of professional users.

- Buyers are expected to maintain existing relationships, build new supplier relationships, and to manage competitive bidding efforts including RFI, RFQ, RFPs and vendor negotiations.

- This is a global role, with responsibility to support multiple international business units and travel internationally.

ToughBuilt is David competing against Goliath

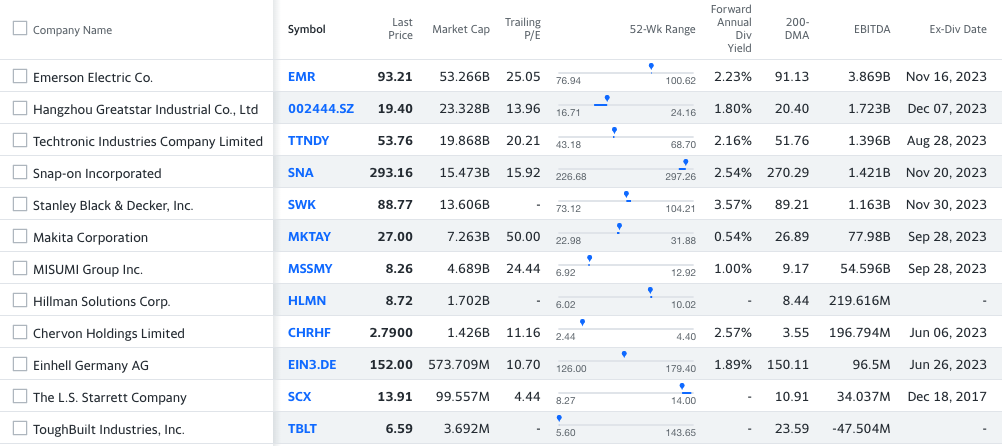

ToughBuilt has many competitors who are significantly larger and better capitalized.

Primary Competitors:

Competition Insights:

ToughBuilt has many competitors who are significantly larger and better capitalized.

- Their competitors dominate tool and accessory retailers.

- Their competitors have a history of tool brand acquisitions.

- Their competitors have a wider selection of products, including power tools.

Primary Competitors:

- Techtronic Industries (Milwaukee Tools, Ryobi, Ridgid)

- Snap-on Incorporated (Snap-On)

- Stanley Black & Decker (Dewalt, Craftsman, Black & Decker)

- Bosch (Bosch, Diablo, Dremel)

- Chervon (EGO, SKIL, Flex)

Competition Insights:

- This is a profitable industry that favors the largest companies. Most large competitors have positive earnings, pay dividends and enjoy high PE ratios.

- Competitor equity market capitalizations are in single or double-digit billions (vs. ToughBuilt in millions)

Source: Yahoo Finance February 5, 2024

Industry Performance

ToughBuilt Industries competes in the DIY and Professional (PRO) tools and accessories markets. As they sell most of their products in home improvement retail stores (Lowe's, Ace Hardware and Home Depot, and brick & mortar retailers in Europe and Latin/South America). They also sell their products online on Amazon, eBay, and through online stores of their retail partners.

The industry is riding a downturn expected to bottom in Q3 2024. The causes will be falling long-term interest rates and mortgage rates, and a consumer sentiment shift back to investing in the home. Until that time, ToughBuilt will grow by taking market share as opposed to riding a home improvement upturn. We believe they can do it with their broad product lineup.

We track Home Depot and Lowe's performance in their public earnings releases and calls. Here is what we see:

1. Q4 was very weak for home improvement, primarily due to fewer large home improvement projects and flat PRO backlogs.

2. January 2024 was weak for home improvement due to extreme U.S. weather

3. The sector declines are due primarily to consumer shift to experiences from goods (e.g., travel and dining), and slow home sales. This is a downtrend that has not yet reached rock-bottom. Home Depot is calling an upturn in H2 2024, and Lowe's says we may have an upturn in H2 2024, but is not counting on it.

We may also see this in earnings calls from direct competitors, but would expect the net-net to be the same.

ToughBuilt Industries competes in the DIY and Professional (PRO) tools and accessories markets. As they sell most of their products in home improvement retail stores (Lowe's, Ace Hardware and Home Depot, and brick & mortar retailers in Europe and Latin/South America). They also sell their products online on Amazon, eBay, and through online stores of their retail partners.

The industry is riding a downturn expected to bottom in Q3 2024. The causes will be falling long-term interest rates and mortgage rates, and a consumer sentiment shift back to investing in the home. Until that time, ToughBuilt will grow by taking market share as opposed to riding a home improvement upturn. We believe they can do it with their broad product lineup.

We track Home Depot and Lowe's performance in their public earnings releases and calls. Here is what we see:

1. Q4 was very weak for home improvement, primarily due to fewer large home improvement projects and flat PRO backlogs.

2. January 2024 was weak for home improvement due to extreme U.S. weather

3. The sector declines are due primarily to consumer shift to experiences from goods (e.g., travel and dining), and slow home sales. This is a downtrend that has not yet reached rock-bottom. Home Depot is calling an upturn in H2 2024, and Lowe's says we may have an upturn in H2 2024, but is not counting on it.

We may also see this in earnings calls from direct competitors, but would expect the net-net to be the same.

The management team is cutting SG&A costs

Inventory Management:

We did data gathering by shopping at physical stores in Chicagoland and around the country while traveling, along with shopping online. We see explicit choices on where inventory investments are made:

Based on what we can see, the Q2 bet was on selling StackTech and a few key products via Lowe's, initiating new "Hot Buy" sales through Menards, and global expansion.

- Discussed in the Q3 2023 earnings call and 10-Q.

- Evidenced by a lawsuit against ToughBuilt in the Superior Court of California for vacating their offices at 8687 Research Drive, Suites 100, 150 and 250. From the lawsuit, this looks to have cut future SG&A expenses by $2.5mm (through 2027), net settlement costs.

- Two lawsuits were recently settled 'out of court' related to cost cutting efforts. Good news, IMO.

- On June 6, 2024: ToughBuilt settled with Concord Property Development, LLC, for not paying rent for 500 South Main Street, Suite 101, Mooresville, North Carolina in the amount of $666,388.20 to be paid on or before September 30, 2024 in four payments starting on June 30, 2024, with no admission of liability. This is a large, open format, historic building f.k.a. Mooresville Mill, which looks perfect for a second design headquarters.

- On May 29, 2024, ToughBuilt settled with PCS Properties 2, LLC for vacating the property at 8687 Research Drive, Irvine, CA. The settlement amount is not disclosed, but both parties pay their own legal fees and there is no admission of liability.

- They occupy a 15,000 sq. ft. single tenant headquarters at 8669 Research Drive. Irvine, CA, which lease expires March 31, 2025.

- We saw a post about 20 job cuts in 2023 and we see minimal job postings (1 or 2 positions at a time).

- Not sure about product COGS cuts. We read in the latest Registration Statement (February 15, 2024) that all products are manufactured in China, India and the Philippines. We caught a glimpse of a lead from an import/export data services provider that ToughBuilt may be moving some manufacturing to Vietnam from China. This would lower labor costs and import tariffs, but is not supported by company filings. Maybe this effort at cost reduction has been terminated?

Inventory Management:

We did data gathering by shopping at physical stores in Chicagoland and around the country while traveling, along with shopping online. We see explicit choices on where inventory investments are made:

- Inventory levels were declining in Q2 2024 with visible out of stocks at Lowe's for StackTech TM mobile modular storage line. However, inventory is visibly being restocked nationwide for StackTech's initial wave of products. We still see few to none of the second and third wave of products (e.g., 3-drawer box, 3-drawer rolling box, dollys), and they are most often unavailable at Lowe's.

- We see declining levels of ClipTech tool belts, pouches and suspenders, tool bags, and knee pads.

- Hand-tools SKU inventories are down.

- The 1,300 and 1,100 pound capacity saw horses are unavailable everywhere we ship, although we see shipments entering the United States containing the C300, 1,100 pound capacity models.

- We see few heavy-duty rolling tool bags, massive mouth bags, and tool totes.

Based on what we can see, the Q2 bet was on selling StackTech and a few key products via Lowe's, initiating new "Hot Buy" sales through Menards, and global expansion.

Common stock offering completed in February 2024 raised ~$3 million dollars.

ToughBuilt is liquidity constrained. It has an ongoing concern statement in its 10-Q filing. It had $1.8mm in cash on hand on September 30, 2023, and has no access to traditional bank lending (Source: CEO on Q3 2023 earnings call).

ToughBuilt has borrowed via short-term, one-year loans in 2022 and 2023, which are paid back monthly with principal and interest. The May 2024 maturity "May Note" from May 2023 was in the amount of $1,254,000 and bears interest at 9.49%.

In April 2024, the company announced a letter of credit from King Trade Capital for purchase order financing of $30 million dollars, which is a significant boost to their ability to restock retail inventory based on firm purchase orders.

Fresh capital in the millions of dollars can only be raised by achieving profitability (or at least positive cash flow from operations).

The capital stack is as follows:

ToughBuilt is liquidity constrained. It has an ongoing concern statement in its 10-Q filing. It had $1.8mm in cash on hand on September 30, 2023, and has no access to traditional bank lending (Source: CEO on Q3 2023 earnings call).

ToughBuilt has borrowed via short-term, one-year loans in 2022 and 2023, which are paid back monthly with principal and interest. The May 2024 maturity "May Note" from May 2023 was in the amount of $1,254,000 and bears interest at 9.49%.

In April 2024, the company announced a letter of credit from King Trade Capital for purchase order financing of $30 million dollars, which is a significant boost to their ability to restock retail inventory based on firm purchase orders.

Fresh capital in the millions of dollars can only be raised by achieving profitability (or at least positive cash flow from operations).

The capital stack is as follows:

- 1,400,000 outstanding common shares (includes pre-funded warrants)

- 1,100,000 warrants (@ $4.405/share)

- ~$1,300,000 in short-term debt

The Path to Profitability (or EBIT break even)

The entire home improvement industry is in cyclical decline with the rise in mortgage and interest rates.

Our proposed strategy to ToughBuilt is to circle the wagons (cut costs) and aggressively grow revenue in already designed products. For ToughBuilt to reach profitability, or at least EBIT neutrality, it has to both grow revenue and/or shrink expenses.

Path forward to profitability (this is our opinion):

1) If the company maintains their absolute cost position (SG&A and R&D), and their COGS percentage (76.2%), they reach break-even EBIT at a quarterly revenue of $65.3mm.

2) If the company improves COGS to 72.5% and maintains their absolute cost position (SG&A and R&D), they reach break-even EBIT at a quarterly revenue of $56.5mm.

3) If the company reduces SG&A and R&D expenses, it reduces the revenue required to break even.

The entire home improvement industry is in cyclical decline with the rise in mortgage and interest rates.

Our proposed strategy to ToughBuilt is to circle the wagons (cut costs) and aggressively grow revenue in already designed products. For ToughBuilt to reach profitability, or at least EBIT neutrality, it has to both grow revenue and/or shrink expenses.

Path forward to profitability (this is our opinion):

1) If the company maintains their absolute cost position (SG&A and R&D), and their COGS percentage (76.2%), they reach break-even EBIT at a quarterly revenue of $65.3mm.

2) If the company improves COGS to 72.5% and maintains their absolute cost position (SG&A and R&D), they reach break-even EBIT at a quarterly revenue of $56.5mm.

3) If the company reduces SG&A and R&D expenses, it reduces the revenue required to break even.

Social Media Mood

There are a few very angry posters in Reddit, StockTwits and Twitter (now X) that talk down the stock.

Social media coverage of their products is great. We read positive product reviews across the net. Anything about their products seems positive, and the few hiccups that one would expect seem to get handled quickly.

There are a few very angry posters in Reddit, StockTwits and Twitter (now X) that talk down the stock.

Social media coverage of their products is great. We read positive product reviews across the net. Anything about their products seems positive, and the few hiccups that one would expect seem to get handled quickly.

Disclosure: The President, Jeffrey Cohen, has no position in this security.