|

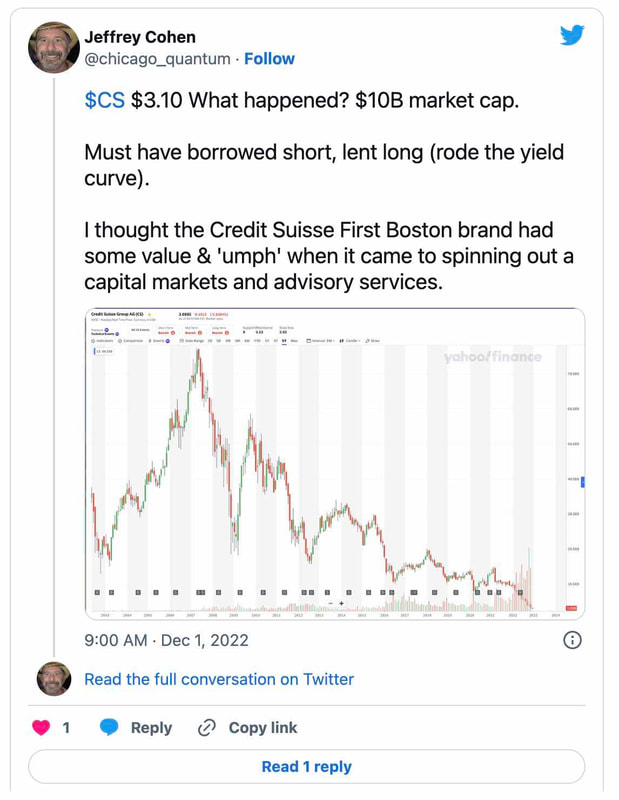

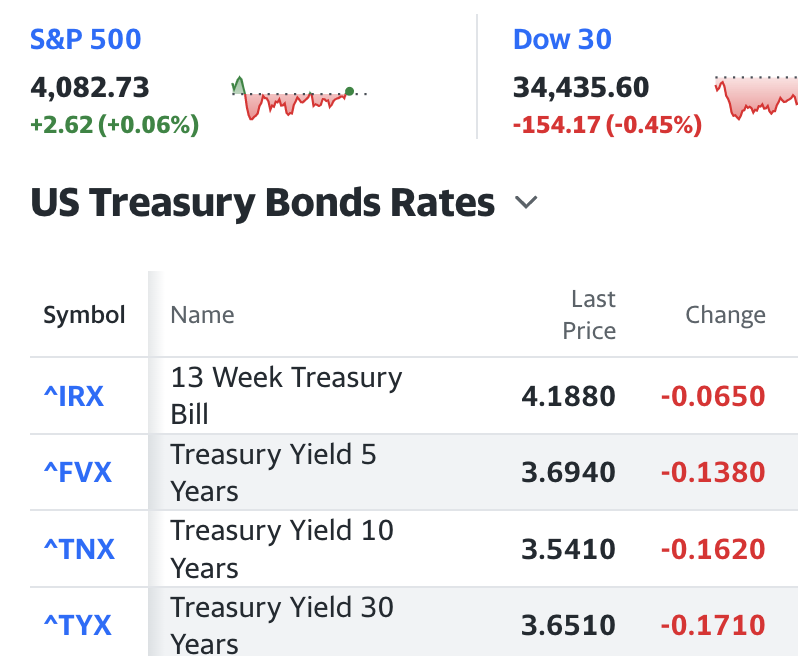

Jeffrey Cohen, US Advanced Computing Infrastructure, Inc Chicago Quantum (SM) What happened today? We made a video to discuss the core economic data we see today. It is all negative and recessionary for the US Consumer and US Manufacturer. Lots of bad news, and a little good news. Tiny good news. So, stocks are pretty strong today...flat...but US Treasury Bond Yields have crashed this afternoon. Good news: GDP grew in Q3/2022 by 2.9% (real) as a revision up from 2.6% (real). Forecasts call for a positive growth rate in Q4/2022. Chicago Business Barometer (TM) from ISM 37.2 (down significantly for 3 months in a row). Lots of bad news in the data for the Midwestern US. Inventory up, orders down, etc. Supplier deliveries down, new orders down, but prices paid are higher (not a joke). ADP Job Increase in November 127k jobs, except that the jobs were in the lowest rungs of the economy and job losses in manufacturing and professional / white collar jobs. Credit Suisse stock hitting an all time low (at least according to Yahoo Finance) and is down 95% from $60 to $3.00. We discuss some potential reasons why. We tweeted on this. Potential BK risk. Saudis and Qataris step in to help rescue the bank.  US Treasury General Account down about $500B this year. This completely offsets quantitative easing by the Federal Reserve Bank. Ouch! The US government collects taxes and this means they likely had to spend it. So, those taxes were not disinflationary after all! BEA: Personal Income and Outlays, October 2022 showed that the US consumer fell behind. It also shows that price inflation slowed slightly. Good news on prices, but bad news on the US consumer. Also, the US savings rate fell to 2.3%, which we believe is very, very low. This couples with retail feedback from companies that are reporting earnings and forward guidance. Costco, Dollar General, Dollar Tree and weeks ago Target are all saying the same thing. More shopping value priced goods. Consumers shopping to their budget, and focusing on core essentials. Also, profits from retail are falling as costs rise. So, it costs more to sell cheaper stuff to consumers who are borrowing money to buy it. Ugh, this is bad news. $COST $DG $DLTR $TGT looks at the news for the details (all from today except TGT). Dollar Tree mentioned they might need to lower prices (what, to back to $1.00?). We slowed down our shopping at Dollar Tree since they raised prices 25% earlier this year. Anecdotally, they tried to sell $3, $4 and $5 frozen food and that seems to have failed at least in our local store (freezers are now empty in those sections). Yesterday, Chair Powell of the Federal Reserve Bank gave a speech. Here is the transcript. We leave it to the actual words spoken, because we struggle to understand the intent behind the talk. It provides transparency, but may have been meant to guide the market and rates. Forward Guidance. Does not seem right that a speech should move markets. Maybe they should stop speaking to the press and public except during FOMC press releases? So much news... Earlier in November the Federal Reserve FOMC released its meeting minutes. We have been reading them and the data on the economy seems to show slowing and weakness. We found it to be very down and negative on economic growth in the USA, and led us to think a recession might be in store for us. This is the data the Fed FOMC had when they raised rates 0.75% last month. So, what are we doing? We have our managed accounts model portfolio in 100% cash right now as the market looks for direction. We are looking into Credit Suisse $CS to see if this could be a bargain purchase (or a short to zero and BK). This could be a waste of time on due diligence, but probably good learning either way.  What about interest rates? We see significant interest rate / yield drops today across the yield curve. 10-year UST down 16.2 basis points. This is a significant move lower.

0 Comments

Leave a Reply. |

Stock Market BLOGJeffrey CohenPresident and Investment Advisor Representative Archives

July 2024

|

RSS Feed

RSS Feed